How to plan a budget

How to plan a Budget

In today’s Australian financial climate—where rising interest rates, persistent inflation, and increasing living costs are putting pressure on households—budgeting isn’t just a good habit, it’s a powerful survival tool. A well-crafted budget gives you clarity and control, helping you track exactly where your money is going and uncover opportunities to save in a time when every dollar counts. It turns uncertainty into strategy, allowing you to stay ahead of expenses, avoid unnecessary debt, and build a financial buffer against unexpected shocks. More than that, budgeting empowers you to make confident decisions about your future—whether that’s investing, buying a home, or simply maintaining peace of mind in a rapidly changing economy. Starting a budget involves understanding your total income, tracking your expenses, and setting realistic financial goals. The process is designed to give you control over your money, reduce financial stress, and help you save.

Here is a step-by-step guide to starting a budget based on expert recommendations:

- Calculate Your Net Income

List all money coming in, including wages/salary (after tax), government payments, and investment income. If your income varies, use an average of the past 3-6 months.

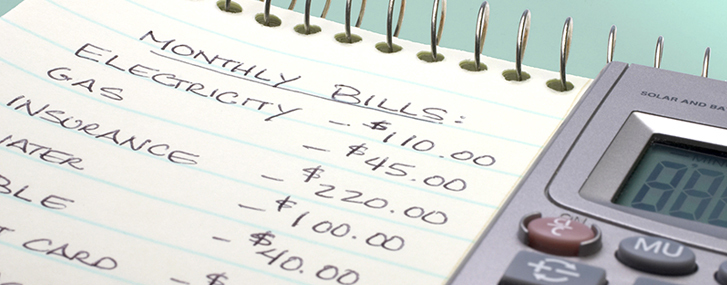

- Track and List All Expenses

Gather bank statements, credit card statements, and bills from the last 90 days to see where your money actually goes. Categorize these expenses:

Financial Advisors Penrith

- Fixed Expenses: Rent/mortgage, insurance, loan repayments, internet, subscriptions.

- Variable Expenses: Groceries, fuel, dining out, entertainment, clothing.

- Periodic Expenses: Quarterly/annual bills like car registration or insurance. Divide these annual costs by 12 and set that amount aside monthly.

- Set Clear Financial Goals

Define what you are saving for, such as an emergency fund (3–6 months of expenses), a vacation, or paying down debt. Having a goal makes it easier to stick to the plan.

- Choose a Budgeting Method

- 50/30/20 Rule: Allocate 50% of income to needs (essentials), 30% to wants (discretionary), and 20% to savings and debt reduction.

- Zero-Based Budget: Every dollar is assigned a job (Income – Expenses = 0). This ensures all money is accounted for and not wasted.

- Pay Yourself First: Automate savings and investments immediately on payday, then spend what remains.

- Review and Adjust

A budget is not "set and forget." Review your spending weekly or monthly to check if you are on track. Adjust categories if you find you are overspending in some areas and underspending in others.

Tips for Success

- Start Simple: If you are overwhelmed, just track every expense for a month before setting strict limits.

- Automate Savings: Set up automatic transfers to a savings account on payday.

- Use Tools: Use budgeting apps (like Frollo or Pocketbook), spreadsheets, or the government-provided Moneysmart Budget Planner.

- Reduce Expenses: Look for ways to save, such as comparing utility providers, reducing food delivery, or cancelling unused subscriptions.